Long-Term Care Awareness Month conversations should always include a mention of the tax advantages of Long-Term Care insurance [LTCi]. For those looking for a last-minute tax deduction, LTCi presents a solution.

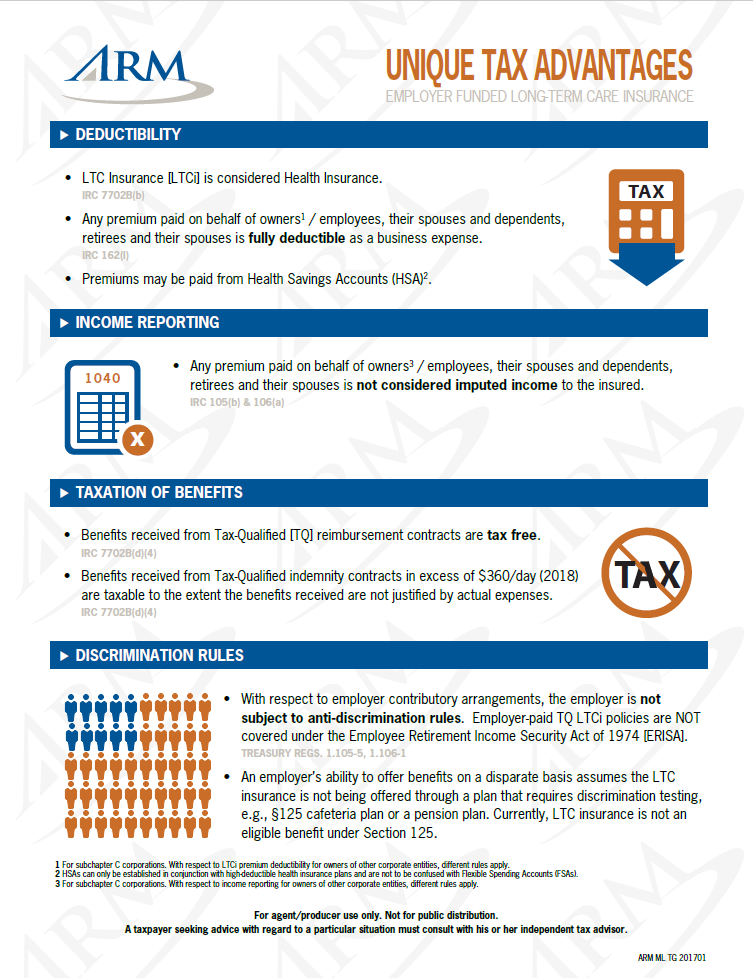

LTCi is considered Health Insurance for tax purposes, which has favorable implications for owners of C-Corporations and S-Corporations alike.

- C-Corporations who fund an LTCi benefit for owners/employees and their spouses or dependents, can fully deduct premiums paid as a business expense

- S-Corporations who purchase LTCi for the owner and their spouse or dependents can deduct premiums up to the federally set Eligible Premium limits

What’s more – regardless of organizational structure, benefits received from an LTCi policy are tax free!

Non-business owners can reap the tax benefits of LTCi policies too. Tax-qualified LTCi premiums can be reimbursed through a Health Savings Account [HSA], tax-free, up to the age based Eligible Premium limits.

See below for the age-based EligiTable Premium limits.

Eligible Premium Limits for 2019

| At age: | You can deduct: |

| 40 & Younger | $420 |

| 41-50 | $790 |

| 51-60 | $1,580 |

| 61-70 | $4220 |

| 71 and older | $5,270 |

-CMYK.png?width=250&name=LifeSecureLogo(F)-CMYK.png)

.png?width=860&height=245&name=Full%20Color%20Krause%20Group%20Horizontal%20(002).png)