Following a period of substantial growth from the 1990s to 2010, Traditional LTC Insurance has encountered difficulties in expanding over the past decade. While sales remain steady, they are not significant enough to address America's Long-Term Care funding crisis. This has been highlighted by various negative press articles, including one from the New York Times' "Dying Broke" series in November 2023.

"Repeated government efforts to create a functioning market for long-term care insurance - or to provide public alternatives - have never taken hold. Today, most insurers have stopped selling stand-alone (i.e. traditional) long-term care policies: The ones that still exist are too expensive for most people. And they have become less affordable each year, with insurers raising premiums higher and higher. Many policyholders face painful choices to pay more, pare benefits, or drop coverage altogether.

As someone who has spent my entire career in LTC Insurance all I can say is - OUCH! That stings because the primary issue with long-term care Insurance has been premium pricing - not the benefit it provides. I say this as someone with personal experience of seeing how LTC Insurance helped both my mother and father-in-law in the last few years - and the pressure it takes off families who are providing care.

But the premiums, in fact, are a large problem with LTC Insurance, affecting both in-force and new policies.

A Brief History of what went wrong with LTC Pricing

A little-known tale from the annals of history reveals that regulators played a significant role in the challenges faced by traditional LTC Insurance. Initially, these policies were bound by minimum loss ratio requirements akin to those found in health insurance. Even though insurance carriers were well aware that these underwritten policies would yield minimal claims during the early years, they were compelled to reduce the initial premium rates in order to meet the loss ratio requirements. This reduction in premiums made the product exceedingly attractive to consumers who could sense an exceptional bargain.

Next, as sales increased with these lower rates and no history of in-force rate increases, carriers and regulators ran into some early indications of upcoming problems with the blocks. This was compounded by the lower-than-expected lapse rates - people wanted to keep this coverage in place! After the 2008 financial crisis, the country also entered a period of ultra-low interest rates - impacting the return insurers had on their reserves.

Seeing the upcoming issues, carriers started to request in-force premium adjustments, but many states stalled on granting those requests due to pressure by politicians or consumers groups. Putting off the painful choices just made things worse when rate increases were finally granted. Also, some states continued to drag their heels on approvals meaning that rate increases were shifted to other states, compounding the bad press around very high premium increases!

A wake-up call occurred when the state of Pennsylvania placed the once high-flying LTC Insurer Penn Treaty into liquidation. (Penn Treaty was a carrier known for low premiums, easy underwriting and high commissions - a recipe for disaster). At this point the National Association of Insurance Commissioners saw the issues related to maintaining the health of in-force LTC blocks as a real crisis that needed to be dealt with before other companies imploded. Rate increases started happening on a frequent basis to the dismay of policyholders and advisors.

At the same time, carriers who remained selling new policies scrambled to offer new products with conservative actuarial assumptions closer to reality. These new products took time to develop and get approved by states. In the meantime, insurance distributors promoted "fire sales" of current generations products - even though they were more likely to receive in-force premium increases in the future than the newer products.

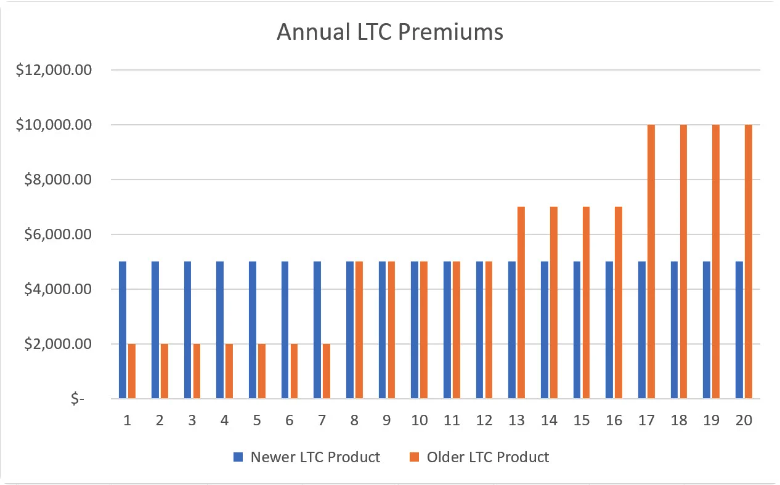

Below is an example of how buying a "fire sale" product may play out. The older LTC policy would have much lower initial premiums but be more susceptible to future rate increases. Meanwhile, the newer product priced with conservative assumptions is much less likely to have future premium increases. In essence, the "rate increases" are baked into initial premiums. For a 55-year-old buyer who needs care at age 75, this person would have paid similar premiums over a lifetime.

However, just because people paid similar total premiums in the above examples does not mean it felt the same. The buyers of the older products who benefitted from lower earlier premiums still felt the pain of the later rate increases - and it has left a bad taste in their mouths.

The ultimate result of this has been class action lawsuits against carriers, upset financial advisors and consumers, and a bad reputation of traditional LTC Insurance in the press.

Enter newer Hybrid Life/LTC Plans

Despite the challenges in the traditional LTC Market, the need for LTC financing remains. Hybrid Life/LTC policies, which have historically been focused on single premium asset-repositioning (think of a CD coming up for renewal), built products that closely resembled traditional LTC plans.

For example, older hybrid plans often had a 100% return of premium feature - if someone changed their mind after owning a plan for a year, they could get all their money back. It ended up that very few buyers decided to give up their valuable LTC benefits, so they were paying for a feature that wasn't used. Newer Hybrid Life/LTC plans have reduced return of premium features in the form of cash surrender values.

Additionally, more and more hybrid policies are sold with longer payment periods - such as up to age 100. These longer pay periods can make premiums more affordable yet still be guaranteed.

New business rates for traditional LTC are conservative - but are they too conservative?

During the last couple of years several of the Hybrid Life/LTC carriers have reduced new business rates - up to 25%. On the other hand, the pricing of traditional coverage has not changed, and carriers haven't reduced new business rates. The result - a side-by-side comparison of premiums and features of these two products is closer than ever.

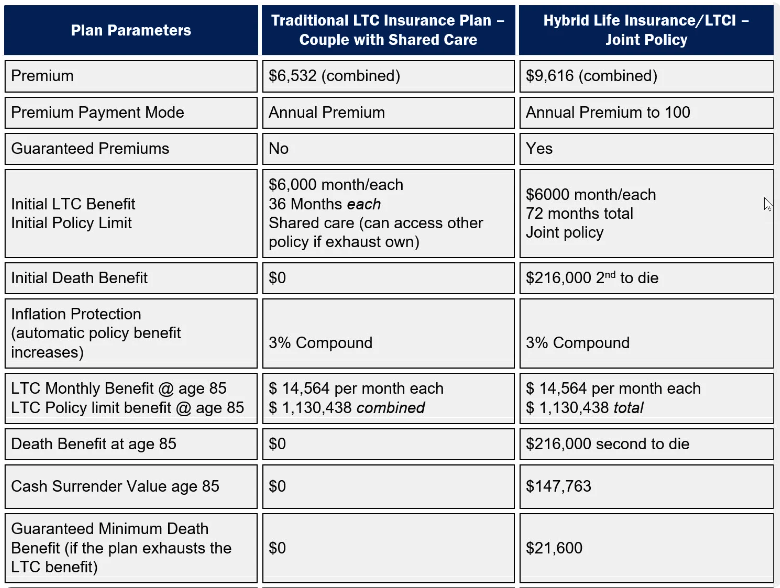

Here's an example of a 55-year-old couple who want an initial benefit of $6,000 per month and 3% compound inflation. They are considering a current traditional LTC plan versus a hybrid life/LTC program.

You could make the argument for either coverage - buyers of the traditional coverage could invest the $3,000 premium savings and probably outperform the $147,000 of cash value in 30 years. On the other hand, the guaranteed premiums plus death benefit make the hybrid option very attractive as well. If I were an actuary at a traditional LTC carrier I may want to think about adjusting new business rates down to be more competitive.

Here are some reasons people may want to consider a traditional long-term care policy:

1. Pure protection for those without need for additional life insurance.

2. Great tax advantages of owning coverage, especially those who are business owners or have Health Savings accounts

3. Ability to dial in affordable premiums but maintain meaningful benefits.

4. Possible ability to avoid taxes on state-based LTC plans such as what happened in Washington State.

5. Ability to qualify for LTC partnership benefits that can help protect assets against Medicaid spend-down.

Yes, there have been real problems with the pricing of traditional LTC Insurance. No one, however, can argue the benefits of owning policies have not been significant. The most recent AALTCI study shared that Traditional LTC Insurance policies have paid out over $14 billion in claims over 2023. As pricing problems have been addressed, this type of policy can be a significant part of a comprehensive financial plan.

-CMYK.png?width=250&name=LifeSecureLogo(F)-CMYK.png)